Kicking off with Using a HELOC to Pay Off High-Interest Debt: Pros and Cons, this opening paragraph is designed to captivate and engage the readers, providing a brief yet intriguing overview of the topic.

Moving on to explain the concept of HELOC and high-interest debt and how they intersect in the realm of personal finance.

Introduction to HELOC and High-Interest Debt

HELOC stands for Home Equity Line of Credit, which is a type of revolving credit that allows homeowners to borrow against the equity in their homes. On the other hand, high-interest debt refers to debts with interest rates significantly higher than average, such as credit card debt, payday loans, or personal loans.

Using a HELOC to pay off high-interest debt involves borrowing money against the equity in your home at a lower interest rate compared to traditional high-interest debt. This strategy can help individuals consolidate their debts into a single monthly payment and potentially save money on interest payments.

Examples of High-Interest Debt Scenarios

- Credit Card Debt: Many individuals carry balances on their credit cards with interest rates ranging from 15% to 25% or even higher. Using a HELOC to pay off this debt can save money on interest payments.

- Payday Loans: Payday loans come with extremely high-interest rates, often exceeding 300% APR. By using a HELOC to pay off payday loans, borrowers can escape the cycle of debt and reduce their overall interest costs.

- Personal Loans: Some personal loans, especially those obtained from online lenders or peer-to-peer platforms, can have interest rates that are much higher than traditional bank loans. Consolidating these loans with a HELOC can lead to substantial interest savings.

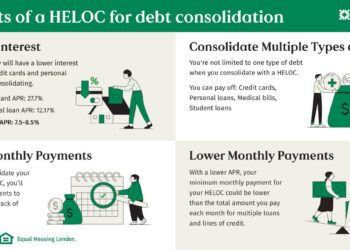

Pros of Using a HELOC to Pay Off High-Interest Debt

When considering using a Home Equity Line of Credit (HELOC) to pay off high-interest debt, there are several advantages to take into account.HELOCs typically offer lower interest rates compared to credit cards or personal loans, making them a cost-effective option for consolidating and paying off high-interest debt. By leveraging the equity in your home, you can access funds at a lower cost, potentially saving you money in the long run.Lower Interest Rates with HELOCs

One of the main benefits of using a HELOC to pay off high-interest debt is the lower interest rates offered by these types of loans. HELOCs are secured by the equity in your home, which reduces the risk for lenders and allows them to offer more favorable interest rates compared to unsecured debt options like credit cards. This can result in significant savings on interest payments over time.Potential Tax Benefits

Another advantage of using a HELOC to pay off high-interest debt is the potential tax benefits. In some cases, the interest paid on a HELOC may be tax-deductible, depending on the specific circumstances and the laws in your country. This can help reduce the overall cost of borrowing and make it a more attractive option for debt consolidation.Flexibility in Repayment Terms

HELOCs offer flexibility in repayment terms, allowing you to tailor your payment schedule to fit your financial situation. You can choose to make interest-only payments during the draw period or make payments towards both the principal and interest. This flexibility can help you manage your debt more effectively and adjust your payments based on your cash flow.Cons of Using a HELOC to Pay Off High-Interest Debt

When considering using a Home Equity Line of Credit (HELOC) to pay off high-interest debt, it is essential to weigh the potential drawbacks. While there are benefits to this approach, there are also risks that need to be taken into account.Risks of Using Home Equity

Using a HELOC means tapping into the equity you have built up in your home. This can put your property at risk if you are unable to make the required paymentsPotential Variable Interest Rates

Unlike a fixed-rate loan, HELOCs often come with variable interest rates. This means that your monthly payments can fluctuate based on market conditions. If interest rates rise, you could end up paying more in interest over time, making it harder to predict and budget for your payments.Possible Impact on Credit Score

When you open a HELOC, it can impact your credit score in several ways. Initially, the credit inquiry and new account can cause a small temporary dip in your score. Additionally, if you max out your HELOC or use a large portion of the available credit, it can increase your credit utilization ratio, which can negatively affect your credit score.Strategies for Using HELOC Wisely

When considering using a HELOC to pay off high-interest debt, it is important to approach it with caution and responsibility. Here are some strategies to help you use a HELOC wisely:

When considering using a HELOC to pay off high-interest debt, it is important to approach it with caution and responsibility. Here are some strategies to help you use a HELOC wisely:Responsible Usage of HELOC

- Only borrow what you need: Resist the temptation to borrow more than necessary, as this can lead to increased debt and financial strain.

- Make timely payments: Be diligent about making your payments on time to avoid penalties and maintain a good credit score.

- Avoid using it for unnecessary expenses: Use the HELOC for debt consolidation purposes only, rather than funding luxuries or non-essential items.

Budgeting Considerations

- Create a repayment plan: Develop a budget that includes paying off the HELOC within a set timeframe to avoid prolonged debt.

- Track your expenses: Monitor your spending habits to ensure you are not overspending and can comfortably repay the HELOC.

- Set aside emergency funds: Have a safety net in place to cover unexpected expenses and prevent relying solely on the HELOC for financial emergencies.

Comparing Different HELOC Offers

- Compare interest rates: Look for the lowest possible interest rate to minimize the cost of borrowing and save money in the long run.

- Consider fees and terms: Evaluate the fees associated with the HELOC and the repayment terms offered by different lenders to choose the most favorable option.

- Read the fine print: Pay attention to any hidden clauses or conditions in the HELOC agreement to avoid surprises later on.

Closing Notes

In conclusion, delving into the world of using a HELOC to pay off high-interest debt reveals both advantages and pitfalls that individuals should carefully consider before making financial decisions.

FAQ Compilation

What are the tax benefits of using a HELOC to pay off high-interest debt?

One potential tax benefit is that the interest paid on a HELOC may be tax-deductible, but it's essential to consult a tax professional for specific advice.

How does using a HELOC impact credit scores?

Using a HELOC can affect credit scores, especially if there are missed payments or high credit utilization, so it's crucial to manage it responsibly.

Are there risks associated with using home equity to pay off debt?

Yes, risks include the possibility of losing your home if you can't repay the HELOC, so it's crucial to weigh the risks carefully.

{kind=link}